This has been a topic that I've been thinking about for quite some time.. and I'd just thought of writing about my thoughts. Inb4 I get flamed by financial advisors/CPF investment platforms.

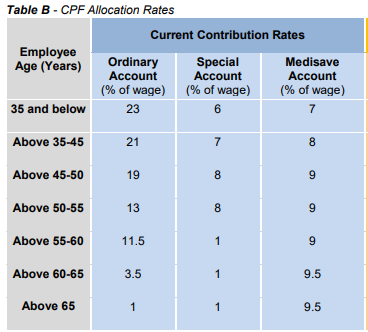

Basically, CPF has a scheme where it allows you to invest using your SA/OA monies, read more about it here. TLDR; you can invest anything above the first SGD20k in OA and SGD40k in SA, ultimately you can just take a look on the CPF platform to see how much you can invest under the "Investment" tab.

Ultimately, this scheme enables financial-savvy you to maximize your retirement amount rather than just earning the basic CPF interests. However, there are very limited things you can invest in as the CPF board tries to limit the investment varieties to the safer ones

This post is actually targeted to spread some awareness for people who are thinking of using your CPF to invest, and there's no one right answer. Different strategies suit different people, but I hope to point out something to make sure most people avoid these!

Bonds and Fixed-Deposit (FD)

In the current low-interest-rate environment, you'll be crazy if you invest in low-yielding instruments such as Singapore government bonds or fixed deposits and forgo your current minimum 2.5% yield.

Equities and Gold

For the more savvy peeps, you'll likely look at equities or even gold to hedge out inflation. Maybe buy DBS and hope it will go up even more in 10 years so you get capital gains along with dividends.

Unit Trusts and ETF

If you're not keen to self-pick, look at unit trusts/ETF that might be performing or has potential.. you will earn gains from payout as well as capital appreciation. This will give you access to invest in instruments that are not available directly to you in CPFIS but you'll be paying very low management/fund fees to the respective unit trust or ETF managers.

Investment-linked Insurance Products (ILP) and Endowment

This is where I want to highlight, insurance products offered by insurance agents/financial advisors..

Honestly, I've not much exposure nor knowledge of this space.. but mostly my take on these. I've friends who taken up normal ILP or endowment plans, and my 2cent after hearing such policies.

While ILP works similarly to normal funds provided by fund managers.. most of such underlying funds in Insurance firms have other fund managers' funds as an underlying component.. which means you're better off investing in the individual funds directly. For example, AIA Global Balance Fund charges you 1.5%pa for you to invest indirectly in; PineBridge (US Large Cap Research Enhanced Fund, International Funds - Singapore Bond Fund), Nikko AM (Shenton Japan Fund), Capital Group (European Growth and Income Fund (Lux)), Legg Mason (Western Asset Global Bond Trust), and Aberdeen Standard (Pacific Equity Fund).

On another note.. Endowment plan's returns are very low mainly because it also has an insurance component.. in my own opinion, one should not mix the two products and such products usually give you half-baked products in both fields.

Endowment plans are actually structured in a very smart way where they give you 2 figures in the investment component; guaranteed return and non-guaranteed return. Usually, these guaranteed returns can be pathetic ~2%pa rate or even worst while the non-guaranteed returns can go up to ~5% or even more... While I personally know some fund managers in insurance firms and they work hard to maximize returns to you.. there's a limitation; investment mandate, market condition, etc, etc..

That's why we've been seeing news on endowment plans holder receive peanuts at the end of the journey.

Summary

For myself.. I look at SA as a safe retirement tool.. ignoring the step-up on the first SGD40k.. you earn a risk-free rate of 4%. Why take the risk of investing even in the safest instrument tool (even the safest tool fail in the worst market), and just let it grow safely in your CPF.

On another hand, for OA.. I take it as my means to pay for a mortgage.. as I rather invest/trade with my readily available cash which I can reap the benefit immediately instead of waiting for god knows how old to withdraw my CPF gains. Sure.. you have accrued interest to pay back CPF.. but if you plan to stay in your home forever.. you will not sell down your property thus no need to pay back the 2.5%.

All-in-all, my belief is when you invest.. it must give you a good return for you to take up the risk.. why give up the safe 4% on your SA and bet on some unreliable endowment plan.. but this is the way of our economy.. to re-package and market the product as something new.

I'd say just leave your CPF alone.. at most I'm moving my OA to SA to make sure I reap more returns. I will also be looking to do voluntary contributions to reduce income tax in the near future when I get paid more..

This is a very brief round-up of such products.. please read up more before taking up any investment schemes and if you have questions or will like me to cover more topics~ shoot it away in the comments

Cheers!