Another month, another tracking.. 1/6 there to annual budget report. Exciting to fill up my tracker up tbh.. hope I'm not the only weird one.

Expense 2021 ~Feb

This month was marginally higher than Jan 2021 despite a shorter month.

While food/groceries fell lower; main contribution was due to Birthday month, so I am paying less for food this month and also shorter month. However, I can see my groceries fee coming up much higher compared to Jan.. mainly due to the fact that I've used up my groceries voucher (was diligently portioning them out). We can expect this category to rise sharply next month due to higher food and groceries costs.. reckon close to SGD1,000.

The rest under Basic remains relatively stable for now, and I also don't foresee any bump coming up for the coming months.

The excess also maintains relatively stable less the entertainment as I had some nights out drinking which explains the higher cost here.

On another note, I've paid to get premium features on my tracking app using money I earned from Google Rewards. I just want to pay back to the service that I've used for more than 4 years. Support what you like before they go under.

Thought of compiling some birthday perks for the month as it is mine this month.. and hopefully will help you uncover some gem that you might have missed.

On second note.. it is quite sad for people to have birthday in February, the shortest month of the year.. meaning you get at least 1~3 days less to enjoy such perks.

Anyway, jumping ahead.. I've split these to a few categories so feel free to jump if the category doesn't interest you.

Personal/Finance

Tiger Broker (Gold Member) - 5 general commission-free trades within 30 days (birthday perks are the same across Silver/Gold/Ace, you just have to graduate from "Uncertified" trader)

Food

Paradise Group (Gourmet Rewards) - 2x rebate throughout the month, meaning a whooping 20% on the subtotal spent

Genki Sushi (Genki Club) - Birthday 20% off nett spend

Shopping

Shopee (Gold Member) - SGD5 voucher on min. SGD10 spending (I think Gold Tier is the only tier with this voucher)

Uniqlo (App Member) - in-store SGD5 off on a min. SGD60 purchase.

BHG (Member) - 20% Birthday Voucher (off regular price items) to redeem at the customer's service counter

Don Don Donki (Bronze Member) - SGD5 off on next purchase (no min. and only during birthday month)

Honestly there aren't much other noteworthy ones such as small promo from qoo10 etc.

Finally my favorite day of the month! Where I compile my expenses and match them to the forecast and see how in-line I am. This month is a good month for expenses even though I restarted working in the office, I'm actually back to a low compared to the last 6 months.

Expense 2021 ~Jan

Special highlights for specific categories..

Food&Groceries

This low figure actually surprised me.. considering my food usually averages around ~SGD1k especially that I need to eat out for lunch working in the office. However, I can expect late next month for my expense in this category to shoot up a little considering that I've been subsidizing my grocery fees with the government-given vouchers.. been using SGD30~40 every weekend. I still have some left for probably the first two weeks of Feb and we can expect to see the expense start crawling up.

Transportation expense is non-negotiable.. however, I always give a little buffer in case I need to take Grab or cab..

The rest of the expenses stay pretty low.. starting the year good.. and I've actually shopped quite a fair bit so this year I don't really have much to splurge on.

My thoughts on CPF might not click with many regular Singaporeans, but on the other hand, I also don’t agree with many financial bloggers who include their CPF in their net-worth since you don’t have liquidity on it (but still it belongs to you, and you need to optimize it for the best performance).

Personally I view CPF as these;

MA is a bonus saving for medical emergencies as well as covering some insurance premium

OA helps with mortgage in the future, however no real point to keep a large sum here

SA best retirement platform which gives yourself a good bonus once you hit 55/65

While many Singaporeans complain about their money being locked up in the CPF, but to be honest, it is the best “force saving” platform that the government has given us along with the amazing interest rate. I also understand the reason why the Government require us to keep a minimum amount to draw out for the rest of our life rather than giving us everything. We can only blame black sheep who can’t manage their finance well in that case (imagine these black sheep draw out all their money, and finish it, it’s us who need to pay for them in the future).

On the other hand, I strongly believe that we should view CPF as a surplus or a bonus rather than it being our net-worth unlike other bloggers because as much as you don’t have access to it, you don’t really own it now (fight me, kidding).

Interest

The key to optimize your CPF starts with understanding the interest rate you’re entitled upon each and every sub accounts. I only plan to go through the “Under 55 Year Old” interest rate, since if you’re above 55, I don’t think there’s much room for you to optimize it.

As many of you know, the interest rate for the following sub accounts are; 2.5%pa for OA, 4%pa for both SA and MA.

There’s an extra 1% on the first $60k balance, this only applies to the first $20k in OA so effectively you can only gain 3.5% on the first $20k and the excess interest actually gets credit into your SA/RA. While the remaining $40k will gain 5%pa can be from your SA and MA (in this exact order).

CPF Plan

CPF Balance

EOY

OA SGD

SA SGD

MA SGD

Total SGD

PSEA

YoY

2018

$ 1,095.85

$ 352.26

$ 1,369.26

$ 10,097.01

$ 7,279.64

0.000%

2019

$ 12,942.01

$ 2,742.92

$ 6,139.91

$ 29,104.48

$ 7,279.64

188.249%

2020

$ 19,550.62

$ 17,411.76

$ 11,774.80

$ 56,558.18

$ 7,821.00

94.328%

CPF as of 3rd Jan 2021

As you can see my CPF started building up in year 2019 because that’s the year I started working, and we can expect YoY growth to slow down. I’ve made a transfer of $10k from my SA to OA which I’ll go through later. In addition, I’ve not touched my PSEA account, so I will be looking forward to it getting transferred to my OA in 2-3 years time.

5 Year Plan

Currently I plan to go along with this plan for the next 5 year as I have my BTO coming in late 2022. As I’ve mentioned I view CPF as a bonus, I plan to continue transferring from my OA to SA to tap on the risk-free higher interest rate (first goal is to hit $40k, but also plan to continue after since 4%>3.5% on the first $20k on OA). I will maintain OA’s balance under $20k for now just to prep my 2nd down-payment for BTO and also future mortgages. In addition, I have the PSEA fund that will be coming soon, which is the main reason why I don’t see a need to maintain a high OA balance.

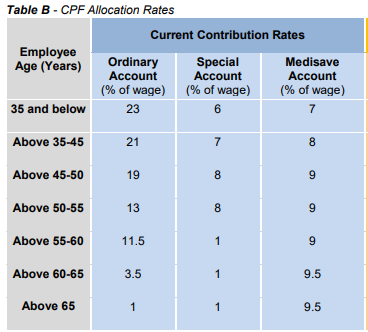

Aside from this, CPF allocation to OA will always be much higher so you have to manually do the adjustment. Do look at the table below for allocation.

This plan might change in the future, most probably after 5 years once my MOP is up and thinking of upgrading to a bigger unit, or even a better location.

Do let me hear about your CPF plan, and if you have any feedback on my strategy/view. In addition, by all means, this only applies to people who are employed with CPF contribution, and I can’t comment for those free-lance people.

As usual, I try to be brief.. if anything you might want to hear more in-depth, feel free to shout out and I might make another post.

Today is actually my favorite day of the year (not my birthday, not any day) but it is not due to being NYE but actually it is the last day of the year.

In Feb 2016, I began my journey to track all my expenses and I’ve been really diligent in doing it, I am proud to say my tracking has minimal error (definitely less than ETF’s tracking, lol). I’ve also progressed slightly as a human, cutting corners on some of the tracking to make my own life easier;

track top-up to Grab wallet as “Food Expense”, save effort on tracking Grab as a separate wallet (inclusive of YouTrip/Revolut/etc)

put aside a small wallet for hawker food where I “top-up” physical cash

no longer count the small cashback/promo on my expense, I just look at it as bonus money in my “Expenditure” bank account

Disclaimer: I don’t track my expenses to limit myself but for me to know where my money is going to, and from there I can forecast a budget for the upcoming year.

Budgeting Excel

In addition to easing my tracking, I also lessen the categories to make life easier thus the above categories. As it is still my first post, I will go through the rationale of my grouping. Basic (Food/Groceries, Transport, House/Personal), I view these as the basic need to my life. While I put the excess (Travel/Entertain, Shopping/Misc) as something that is more controllable. Lastly, I don’t really include Insurance and Mortgage (pardon the typo) into my basic expenses mainly due to I view these as future asset/needs, and by no means have any control in them as well.

Basic (Food/Groceries, Transport, House/Personal)

As you can see that my food/groceries expenses are pretty high, as my current enjoyment in life is mainly in eating (my goal is to go to any restaurant and not care the price tag while ordering), so I’ll allocate high budget to this category; taking into consideration of inflation and increasing standard of living, I accounted for a slight increment.Transport is one of the best performer in the budget but it was due to 3 months worth of Circuit Breaker (Singapore locked down) that I am able to WFH thus transport expense is less than SGD20 in these 3 months; while I budgeted for this year with the thought that I can still buy student concession fare till August, thus I’d keep the same budget for next year and see how it goes. Lastly, on house/personal, it ranges from the monthly contribution I put at home along with personal therapy, medical and etc. However, start of the year was harsh.. as my kitten required some excess vet support which caused it to go over budget (no regret there, hope you’re having fun at the rainbow bridge my lovely kitten) as well as some household goods breaking down; going forward I reckon chances of such one-off expenditure will not incur (touch wood) thus the lower budget.

While I budgeted quite a fair bit of travel, I only managed to visit Johore Bahru (JB) once due to the Covid19 pandemic but I plan to set aside similar budget for next year, hoping that travel might resume in 2021Q3. On another note, my shopping expense has overshot the budget (2 years straight) but this year was mainly due to a one-off purchase of my new phone at SGD1k which I expect to last me for a minimum of 3 years (based on my iPhone 7 lifespan). Honestly I feel that the budget is slightly higher than what I really need, but I’d love to buy things from sales (especially work shirt, etc).

Expense Wrap-Up

This year, surprisingly I am in the green (thanks to Covid19), however I still plan to set aside a higher budget; not to restraint myself too much and I also got a pay bump from job hop. Ultimately, my goal is total less “mortgage&insurance” can factor less than a certain percentage of my basic take-home pay (currently in 40~50% range, not revealing because it will be easy to reverse engineer my gross); goal will be eventually hitting less than 25% of my take home through both way of earning more money and spending less.

“Don’t let what you earn dictates how much you spend” -Me

Tracking App

I understand there’s many apps out there that will help with your tracking including app from Seedly, Gpay (allows you to track all expenses that is paid via card etc), banking apps and etc. Personally I use Monny, I like the flexibility and ease of usage of the app. Few note-worthy points are; allow you to create multiple accounts (for different accounts such as investment/spending/travel expenditure), create of categories, and recurring expenses. You can find the app in the following link – https://play.google.com/store/apps/details?id=com.greamer.monny.android

Disclaimer: I am not sponsored to share the app, nor I will get any referral fees from this.

And Happy New Year to everyone, hopefully 2021 will be a better year to achieve all of our goals!