My thoughts on CPF might not click with many regular Singaporeans, but on the other hand, I also don’t agree with many financial bloggers who include their CPF in their net-worth since you don’t have liquidity on it (but still it belongs to you, and you need to optimize it for the best performance).

Personally I view CPF as these;

- MA is a bonus saving for medical emergencies as well as covering some insurance premium

- OA helps with mortgage in the future, however no real point to keep a large sum here

- SA best retirement platform which gives yourself a good bonus once you hit 55/65

While many Singaporeans complain about their money being locked up in the CPF, but to be honest, it is the best “force saving” platform that the government has given us along with the amazing interest rate. I also understand the reason why the Government require us to keep a minimum amount to draw out for the rest of our life rather than giving us everything. We can only blame black sheep who can’t manage their finance well in that case (imagine these black sheep draw out all their money, and finish it, it’s us who need to pay for them in the future).

On the other hand, I strongly believe that we should view CPF as a surplus or a bonus rather than it being our net-worth unlike other bloggers because as much as you don’t have access to it, you don’t really own it now (fight me, kidding).

Interest

The key to optimize your CPF starts with understanding the interest rate you’re entitled upon each and every sub accounts. I only plan to go through the “Under 55 Year Old” interest rate, since if you’re above 55, I don’t think there’s much room for you to optimize it.

As many of you know, the interest rate for the following sub accounts are; 2.5%pa for OA, 4%pa for both SA and MA.

There’s an extra 1% on the first $60k balance, this only applies to the first $20k in OA so effectively you can only gain 3.5% on the first $20k and the excess interest actually gets credit into your SA/RA. While the remaining $40k will gain 5%pa can be from your SA and MA (in this exact order).

CPF Plan

| CPF Balance | ||||||

| EOY | OA SGD | SA SGD | MA SGD | Total SGD | PSEA | YoY |

| 2018 | $ 1,095.85 | $ 352.26 | $ 1,369.26 | $ 10,097.01 | $ 7,279.64 | 0.000% |

| 2019 | $ 12,942.01 | $ 2,742.92 | $ 6,139.91 | $ 29,104.48 | $ 7,279.64 | 188.249% |

| 2020 | $ 19,550.62 | $ 17,411.76 | $ 11,774.80 | $ 56,558.18 | $ 7,821.00 | 94.328% |

As you can see my CPF started building up in year 2019 because that’s the year I started working, and we can expect YoY growth to slow down. I’ve made a transfer of $10k from my SA to OA which I’ll go through later. In addition, I’ve not touched my PSEA account, so I will be looking forward to it getting transferred to my OA in 2-3 years time.

5 Year Plan

Currently I plan to go along with this plan for the next 5 year as I have my BTO coming in late 2022. As I’ve mentioned I view CPF as a bonus, I plan to continue transferring from my OA to SA to tap on the risk-free higher interest rate (first goal is to hit $40k, but also plan to continue after since 4%>3.5% on the first $20k on OA). I will maintain OA’s balance under $20k for now just to prep my 2nd down-payment for BTO and also future mortgages. In addition, I have the PSEA fund that will be coming soon, which is the main reason why I don’t see a need to maintain a high OA balance.

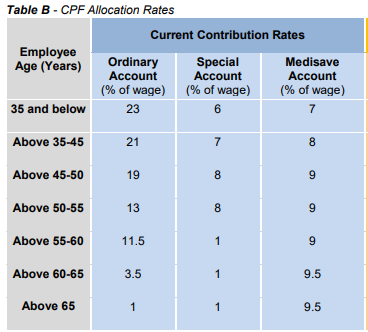

Aside from this, CPF allocation to OA will always be much higher so you have to manually do the adjustment. Do look at the table below for allocation.

This plan might change in the future, most probably after 5 years once my MOP is up and thinking of upgrading to a bigger unit, or even a better location.

Do let me hear about your CPF plan, and if you have any feedback on my strategy/view. In addition, by all means, this only applies to people who are employed with CPF contribution, and I can’t comment for those free-lance people.

As usual, I try to be brief.. if anything you might want to hear more in-depth, feel free to shout out and I might make another post.

No comments:

Post a Comment